Share and Follow

SPDR S&P Regional Banking ETF

Universal Value visors

Despite ongoing silent runs on the Regional and Community Banks, it appears that both Fed Chair Powell and Treasury Secretary Yellen view the events of the recent past (SVB

VB

, Signature Bank, First Republic, Credit Suisse, and now Deutsche Bank) as one-off events and not symptomatic of stress in the world’s financial system. The dictionary defines “obtuse” as “annoyingly insensitive or slow to understand.” We can’t think of anything more precise!

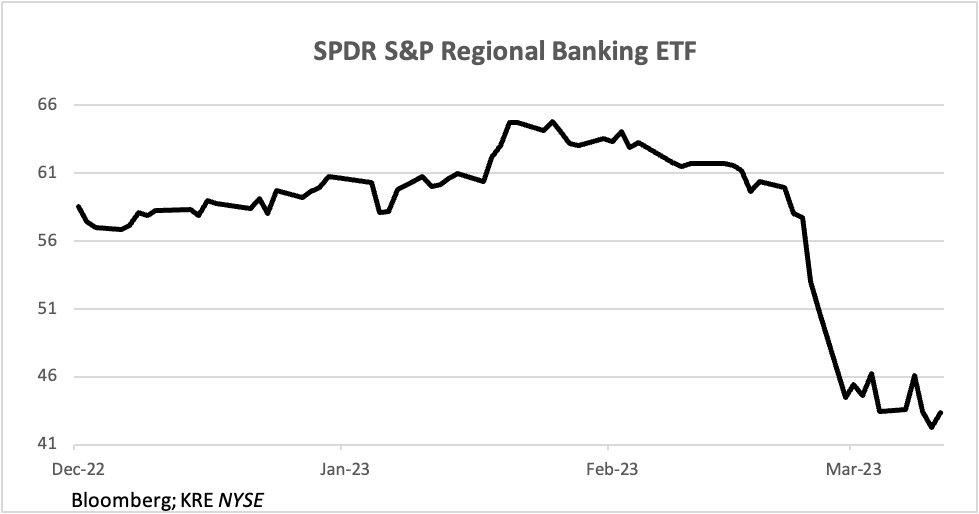

The chart at the top shows the continued decline in the value of S&P’s Regional Banking ETF through the close of business on Friday (March 24th). On Wednesday, the Fed raised interest rates 25 basis points despite liquidity issues in the banking system and the apparent loss of confidence in that system by a significant portion of the public. During his press conference, Powell acknowledged some FOMC concerns over banking issues, said that they had considered a “pause,” but concluded that a rate hike was justified due to the strength of recent economic activity, higher than expected inflation data, and the fact that “deposit flows had stabilized.” There was no acknowledgement that the stresses were continuing.

The fact that the FOMC had discussed “pausing” caused the equity market to initially rally. However, a few minutes later, at a Congressional hearing, Treasury Secretary Yellen undid it all and then some by telling lawmakers that Treasury was “not considering a broad increase in deposit insurance.” (Translation: We will cover 100% of deposits at big banks; good luck to you smaller guys!) The chart shows equity market reactions, first to the less hawkish Powell, then the massive sell-off when Yellen dissed the small banks. The next day (Thursday, March 23) she qualified her statement by saying that 100% of the deposits would be covered if the bank was “systemically important” (still dissing small banks).

Market Sensitivity to Fed/Treasury Comments

Zerohedge

Silent Runs Continue

As a result, there has been a continuation of the silent run on small bank deposits. From the charts below, we can see that banks borrowed approximately $350 billion from the Fed over the past two weeks. The left side shows borrowings rising from about $20 billion to $350 billion.

Discount Window Borrowing & 2023 Supplying Reserve Funds

Universal Value advisors

The right side shows the Fed’s balance sheet bloating from $8.39 trillion to $8.74 trillion (about $350 billion).

The New Dot-Plot

The March Fed meeting produced the quarterly “dot-plot,” i.e., the forward interest rate opinions of 18 FOMC members. Despite the banking woes and mounting evidence of a rapidly slowing economy, there was only one dot that was below the 5% line for 12/31/23, with 10 dots at 5.1% and the other seven somewhat higher. Perhaps this was meant to tell the public that the Fed was serious about its inflation mandate, as it certainly doesn’t comport with the market’s view of economic reality. The chart below shows the market’s March 1st and March 24th views of where rates will be as 2023 progresses. Note how the market’s view of rates change from prior to the banking issues (blue bars) to after (gold bars). The blue bars are very close to both the FOMC’s December and March dot-plots. Markets now see a “pause” in May, a “pivot” in June with rate reductions continuing at each meeting through next January. Clearly, market participants see a very different economic picture than does the Fed or the Treasury. Which do you believe?

Fed Funds Futures

Universal Value visors

Who’s to Blame?

Part of the problem is that Fed and Treasury do not appear to see their role in the unfolding banking crisis. There are several issues here:

- The first is the potential insolvencies of some banks. Note, this is not all, and likely a minority, but still concerning. The chart below shows gains and losses in bank bond portfolios. The large losses on the right-hand side are directly related to Fed interest rate increases since March 2022. Because of accounting rules for banks, such losses do not have to be recognized unless bonds are sold. In the case of SVB, the bonds had to be sold because SVB did not have sufficient time to arrange for borrowing. The realized losses ate through SVB’s capital and caused its insolvency.

Net Unrealized Gains in Bank Bond Portfolios

Read Related Also: Biden Has Skin Cancer Cell Removed Following Same Operation On First Lady

FDIC, Capital Economics

- To temporarily halt the sale of bonds at banks (i.e., and protecting their accounting capital level), the Fed established the “Bank Term Funding Program” (BTFP) which allows banks to borrow using bond collateral at face value rather than at market value. In this way, banks could get more cash for their bonds than they are worth without having to sell them and take the write-down on their balance sheet and income statement. (What a great way for regulators to turn a blind eye to the reality that capital is much lower than the accounting statements would have one believe!) While small banks now have a short-term life line, it is the long-term issues of small bank survival that appears to be out of mind at both the Fed (raising rates further) and Treasury (giving 100% FDIC coverage to large banks but not small ones).

- Big banks will survive and prosper as they now are the recipients of new, low/no cost deposits that have abandoned small banks where insurance ceilings remain.

- The small banks have now borrowed huge sums of money at a 4.75%-5.00% interest rate (the Fed Funds Rate) pledging a portfolio of bonds likely yielding less than 3%. That kills profit margins, as those bonds were previously financed with no or low-cost deposits. And even if this crisis passes, banks are going to have to pay market rates for deposits to return, again something that will crip their profits.

- The liquidity situation at small banks is such that new lending is a non-starter. They need an influx of new deposits, something that won’t happen for a significant period of time. Small banks have always been the primary lenders to small businesses in their local communities. So, today’s situation has serious negative implications for economic growth in the economy going forward.

- In addition, small and mid-sized banks hold a huge 58% of Commercial Real Estate (CRE) loans. We have noted in past blogs that office complexes in NYC and L.A. have gone into foreclosure. The work from home trend isn’t going away, and this implies an oversupply of office space with serious implications for small banks, for their future earnings, their loan losses, and their capital.

Even prior to the crisis in confidence, banks were losing deposits to money market funds where overnight yields were much higher (right-hand side of chart). And, as we have noted in past blogs, for some time, banks have been tightening lending standards (left-hand side of chart).

Commercial Bank Credit and Deposits

Universal Value visors

Powell was asked about this at his press conference, but he blew it off saying he didn’t see it as analogous to the current liquidity issue. And while we agree that it isn’t analogous, it is a serious issue worthy of discussion.

And so, as Nero (Powell) fiddles, Rome (small banks) burns!

Inflation?

As noted, the Fed believes that the economy is strong and that inflation is endemic. The reason for this is their reliance on lagging indicators, like year/year inflation rates and the unemployment rate (the most lagging economic indicator of them all). While year/year inflation is 6%, it has come down quite rapidly from nearly 9%, and, over the last three months, the CPI has risen at an annual rate of just 2.1%, right at the Fed’s target. Commodity prices peaked nine months ago (June, 2022) and the price of crude oil, which was over $120/bbl. back then is now trading at $69/bbl. Does the chart below look inflationary to you?

CRB Commodity Index

Commodity Research Bureau BLS/US Spot All Commodities

Layoffs

In past blogs, we enumerated some of the large layoff announcements. They have continued now in the consultant/accountant arena: Accenture

ACN

(19,000), McKinsey (2,000), KMPG (700), E&Y (thousands). And also, in employment companies (when the head hunters cut their own heads, you know something is wrong!) – Indeed (2,200). As we noted in our last blog, the WARN Act (1980s) requires 90-day layoff notices for large layoffs (180 days in CA) prior to separation, so those Q4 layoff announcements will soon begin to show up in the unemployment data. We saw the first installment of this in February’s U3 unemployment rate, rising to 3.6% from 3.4% in January.

Final Thoughts

The Fed’s own Regional Bank Surveys all point to significant economic slowing. Orders and backlogs have fallen for several months, prices have been weakening, and the overall indexes are contracting. Yet, into the storm of a distressed banking system, both at home and abroad, clearly caused by sky high interest rates, what does this Fed do? Raise them even higher!!!

And what does the Treasury Secretary say? While big bank deposits are 100% guaranteed, best of luck to you little guys!

Obtuse is the best descriptor we can find.

(Joshua Barone contributed to this blog)