Share and Follow

Reflecting on his decision to purchase a four-bedroom house in Perth five years ago, Oliver Barley considers himself fortunate. At the age of 33, he bought the property for $780,000 during the turbulent period of the COVID-19 pandemic. Fast forward to today, and the same house is now valued between $1.2 million and $1.4 million.

“I don’t think we could afford to buy our house currently,” Barley admits to SBS News, acknowledging the financial strain that a mortgage would impose, particularly as his wife is currently on maternity leave. The significant appreciation in the property’s value has left him both surprised and concerned.

Barley’s astonishment at the rising value of his home since 2021 is coupled with a sense of urgency for change. He observes a pervasive sense of pessimism among his friends regarding the housing market and their future prospects, highlighting a broader sentiment of uncertainty and unease.

Barley says he was astonished to find out how much his property has increased in value since 2021, and he believes change is necessary:

I think we’ve reached what is very clearly a breaking point and a level of inequity that is no longer feasible.

He says all of his friends feel extremely pessimistic about the housing market and what their future ultimately looks like.

“The numbers just don’t work,” Barley says.

“Those who didn’t get on the housing market are now just looking at it as a ship that has sailed.”

With housing increasingly out of reach for young people, experts are now raising concerns that Australia’s taxation system could be fuelling inequality — and unfairly benefiting older Australians.

Australia’s tax system is set up for ‘wealth creation’

For decades, Australia has provided financial support to older residents as they retire and their incomes drop.

But spending per person on the age pension, aged care and health care has increased significantly in the last 30 years, while expenditure targeting younger households has remained relatively constant.

Generous tax arrangements have also allowed older Australians to accumulate significant wealth and income linked to their real estate and superannuation assets.

Despite this growing wealth, the tax system has not adjusted, instead providing increased support for older generations, a working paper from the Australian National University’s (ANU) Tax and Transfer Policy Institute last year found.

The impact of tax concessions can be seen in the post-tax income of older Australians.

The report noted that, in the decade between 2013/14 and 2022/23, post-tax income for the over-60s was almost equal to that of younger cohorts.

That’s despite many over-60s being retired or nearing retirement, and their before-tax income being substantially less than that of younger Australians.

The before-tax income of older Australians was 65 per cent of that earned by younger people, but rose to 95 per cent after tax due to the generous concessions.

“Current settings increasingly favour older Australians at the expense of younger Australians,” the report notes.

However, ANU economic and social researcher Ben Phillips notes that not every older Australian is wealthy and, despite concessions, some would be struggling.

A couple who owns their home still needs a combined $730,000 in super to enjoy a comfortable retirement, according to the Association of Superannuation Funds of Australia.

Around 92 per cent of Australians with super had a balance of less than $500,000 in 2022/23, according to data collected by the Australian Tax Office.

Phillips says tax concessions such as those for negative gearing, capital gains and superannuation have some legitimacy, but he believes Australia is too generous, especially when it comes to super.

He notes the largest benefits flow to those with the biggest super accounts and substantial property holdings.

We do see this increasing gap where it’s older Australians getting richer.

Property prices in Australia have skyrocketed over the last 40 years, with a PropTrack study last year showing Sydney properties were four times higher than in 1980, adjusting for inflation.

This means a typical house cost $65,000 in 1980, which would be roughly $338,000 in today’s money.

The staggering rise in property prices — with houses in Sydney typically selling for $1.47 million last year — is putting money into the pockets of those lucky enough to have bought earlier, while locking out younger generations.

“I think at the moment with the tax system in Australia, it’s pretty well set up for wealth creation,” Phillips says.

‘Levelling the playing field’

Phillips believes Australia needs to change its tax system to rein in generous concessions that generally benefit older cohorts.

But he says this does not have to involve increasing taxes overall.

“It’s probably about rebalancing how we tax in Australia,” he says.

If you lower the tax concessions [such as negative gearing, capital gains and superannuation], it does allow you to start doing things like lowering personal income tax.

Economist Chris Richardson of Rich Insight believes Australia has made two big policy mistakes — both of which have hurt the young while benefiting older Australians.

They centre on two areas where most of the nation’s wealth is held: housing and, to a lesser extent, the share markets.

Richardson notes Australia is more generous with retirement support for wealthier residents through super tax concessions, for example, than it is for those on low incomes.

He says changing these arrangements is not about being “unfair to older and richer Australians”.

“What we are doing is spectacularly unfair and comes at a pretty massive cost. So a little touch of fairness would be a grand thing,” he says.

“We’re levelling a playing field which is dangerously tilted and absolutely worsens inequality.”

Comfortable in old age, struggling in middle age

As Phillips points out, financial stress tends to be highest among younger and middle-aged Australians.

According to the latest Household, Income and Labour Dynamics in Australia survey released in December, people aged 65 and over consistently report the lowest levels of financial stress, with 6 per cent saying they were stressed in 2023.

This compares to 14 per cent of younger cohorts.

Phillips says just because someone has turned 60, it doesn’t mean they suddenly have the right to pay no tax (apart from GST on things they buy).

There should be some [concessions but] at the moment you’ve got extremely wealthy households who are over the age of 60, who are paying not a cent of tax on their earnings.

“I think that’s grossly unfair, and I think it puts a bit too much burden on younger families, who we do know are actually struggling.”

Experts also warn that as Australia’s population ages, a smaller proportion of young people will be expected to support older generations.

By 2050, there could be just 2.7 people of working age for each person aged 65 years or older, compared with five people in 2009, and 7.5 people in 1969, according to the Rudd government-commissioned Henry tax review published in 2010.

Phillips says Australia may have to increase taxes to support its ageing population due to higher aged care and pension costs.

If so, he believes it would be fairer to reduce tax concessions on superannuation rather than squeeze more money out of people who pay income tax.

Over the past 15 years, Australia has increased taxes through bracket creep — meaning workers pay more as inflation pushes them into higher tax brackets.

What taxes could be changed?

Phillips says superannuation concessions would be the most important area for change.

Once Australians retire, they can still have up to $2 million in a super account and pay no tax on the income it earns.

If it’s invested in a balanced fund with returns of 5-6 per cent, they could be earning around $100,000 a year tax-free.

A couple would then have a combined amount of $4 million, allowing them to earn up to $300,000 a year tax-free (if invested in a fund with returns of 7-8 per cent).

“That’s unnecessarily concessional,” Phillips says.

“If you were a 40-year-old and you’re earning $100,000 a year and looking after a couple of kids … you’d be paying 32.5 cents in the dollar [for a tax bill of around $22,967].”

‘Takes money from the poor and gives it to the rich’

High-income earners are also the biggest beneficiaries of how money transferred into super is taxed.

“It takes money from the poor and gives it to the rich,” Richardson says of the current super arrangements.

“On average, that means taking money from the young and giving it to the older.”

Super contributions are taxed at 15 per cent (up to an amount of $30,000) — which is 30 percentage points below the top income tax bracket of 45 cents in the dollar, but just 15 points lower than what many middle-income earners pay.

Richardson notes these generous super concessions don’t save Australia much when it comes to funding the age pension.

“That’s a myth,” he says.

“So we have it wrong, pure and simple.”

Richardson says one of the recommendations in the Henry tax review, which he supports, is changing the superannuation rules so everyone gets the same discount.

A tax discount of 15 percentage points, for example, would allow someone in the top tax bracket (of 45 cents in the dollar) to bring their rate down to 30 cents. Someone in the 32.5 per cent bracket would pay 17.5 cents per dollar.

This allows everyone to gain the same benefit.

Previously, super funds complained that implementing this would be administratively complicated, but Richardson says technology has improved since the 1990s.

Options being considered by government

Treasurer Jim Chalmers has acknowledged “intergenerational issues in the tax system and in housing”.

A Senate inquiry was established last year into the operation of the capital gains tax (CGT) discount, with a report due on 17 March.

The CGT discount is applied when you sell assets that you have owned for at least a year — including stocks, jewellery and properties.

It allows you to claim a 50 per cent discount on tax paid on the profit.

Chalmers told ABC RN Breakfast on 26 February that the government hasn’t changed its policy despite reporting from the Australian Financial Review suggesting Treasury is considering a reduction in the CGT deduction from 50 per cent to 33 per cent.

New rules to limit negative gearing to two investment properties are also being examined, according to reports in The Australian.

Chalmers says the government has tried to address affordability issues by building more homes and offering 5 per cent deposit guarantees for first-home buyers.

But he acknowledges there are other options being considered as part of the budget, which is due to be handed down in May.

Opposition leader Angus Taylor told 2GB last Friday it’s “highly unlikely” he would support changes to negative gearing or the CGT because “we want to see more houses”.

Last year, the government also introduced legislation to double the tax rate on earnings for superannuation funds of more than $3 million — to 30 per cent — but this has not yet been passed by the Senate.

It will also introduce a new 40 per cent tax for balances above $10 million.

Housing reform also needed

Experts acknowledge that reforming negative gearing and the CGT won’t solve the housing affordability problem, but would likely slow price growth.

Richardson says CGT changes being debated might dampen property prices by 1.5-2 per cent, which would have a similar impact to the Reserve Bank lifting rates by 0.25 percentage points.

Regardless, Richardson does think the tax needs to be changed.

“Because we can have a better tax, not because it’s a magic solution in housing,” he explains.

Richardson believes other changes, such as reforms to planning regulations, will also be necessary to bring down house prices.

“For 40 years in Australia, our housing policy has been the word ‘no’. It needs to change to the word ‘yes’,” he says.

He says housing affordability is a complex problem and it will be a “battle that will be fought for decades”.

Victoria provides hope for aspiring homeowners

Barley remains hopeful change can happen and points to Victoria, which appears to have cooled its housing market.

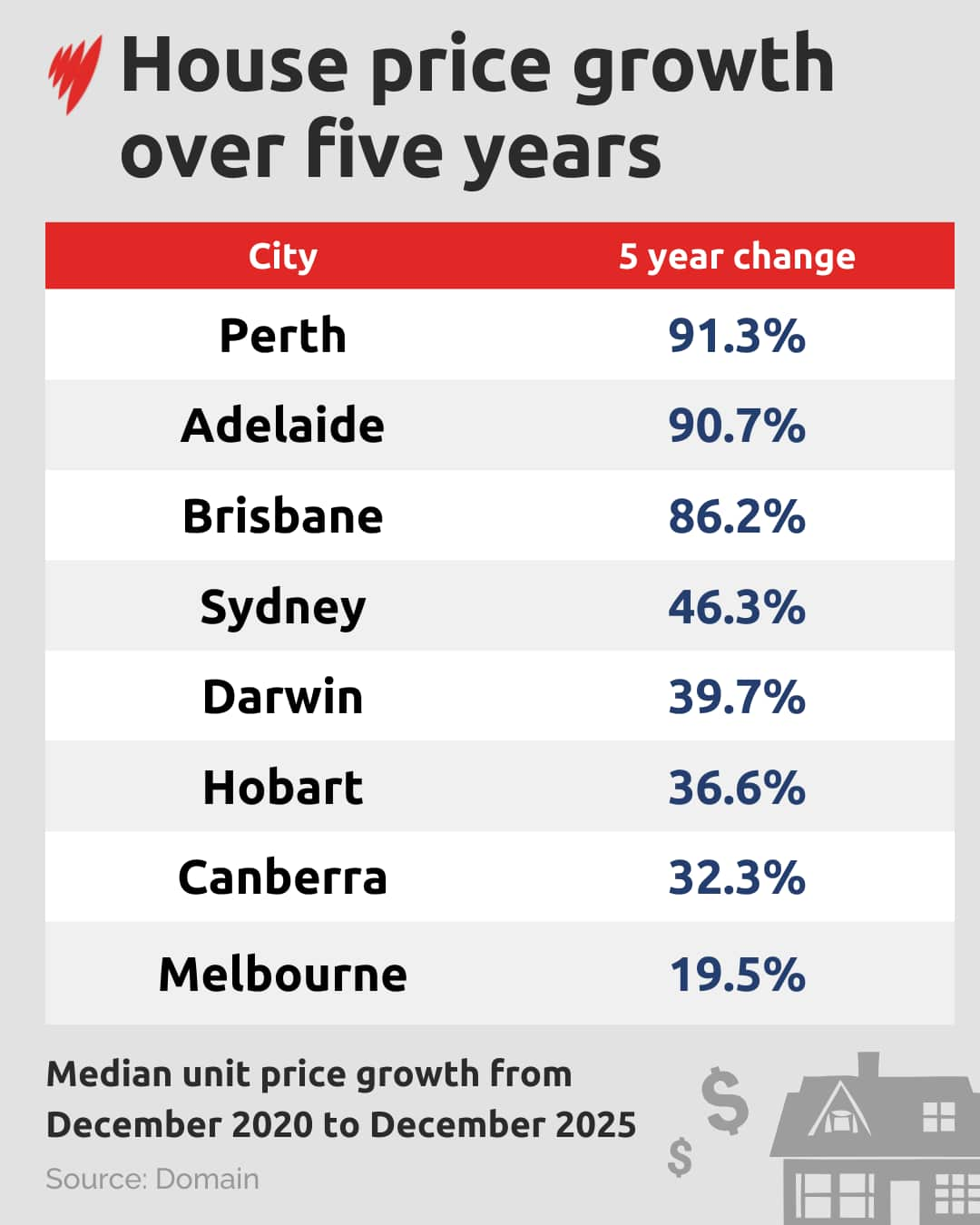

Data supplied to SBS News from Domain shows property values in Melbourne are growing at the slowest rate of all capital cities.

In the five years from December 2020 to December 2025, house prices in Melbourne grew by 19.5 per cent — much lower than the growth in Perth (91.3 per cent), Adelaide (90.7 per cent), Brisbane (86. 2 per cent) and Sydney (46.3 per cent).

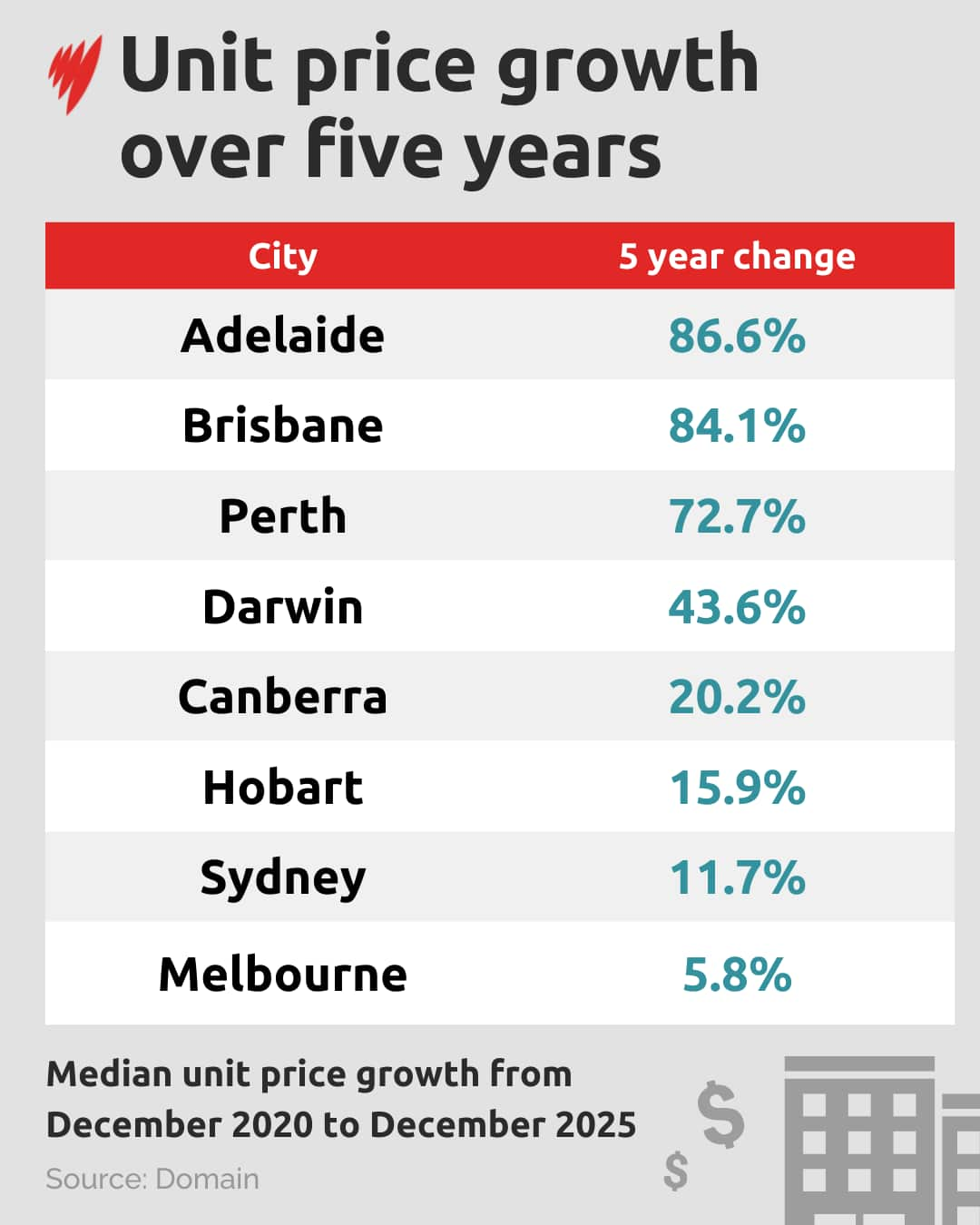

Unit prices rose by only 5.8 per cent in Melbourne, compared with 86.6 per cent in Adelaide.

Changes to tax policies in Victoria have made it less appealing to investors, including forcing more homeowners generating an income from their property (through Airbnb, for example) to pay land tax.

Kate Raynor, an urban planning expert with public policy think tank Per Capita, told SBS News earlier this year that Victoria also approves more new homes than other Australian states and territories.

“I would definitely be in support of changes similar to those [in Victoria],” Barley says.

He also supports changes to the capital gains discount but fears incendiary commentary over even the most modest changes.

“It doesn’t seem like we can have a reasonable conversation about this because the extremes just get pushed so hard.”

For the latest from SBS News, download our app and subscribe to our newsletter.