Share and Follow

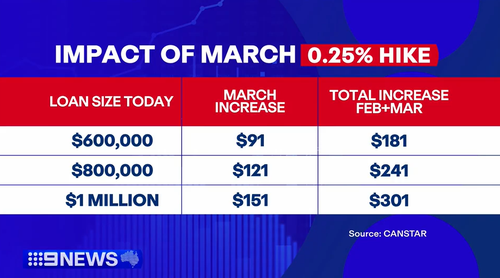

Last week, the Reserve Bank of Australia (RBA) raised the official cash rate to 4.10 percent, marking an increase of 0.25 percentage points. This adjustment has already had a ripple effect on mortgage rates.

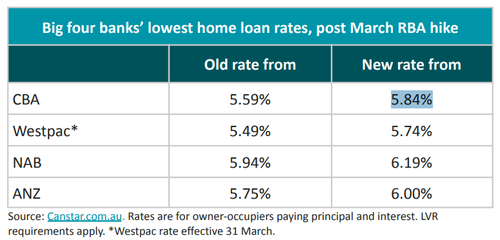

This morning, borrowers with variable-rate mortgages from major banks such as Commonwealth Bank of Australia (CBA), National Australia Bank (NAB), and Australia and New Zealand Banking Group (ANZ) witnessed an uptick in their interest rates.

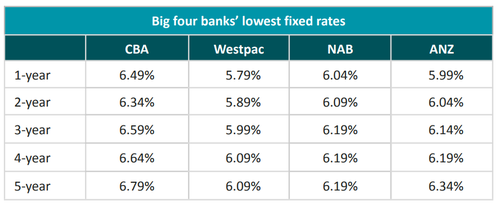

In addition to the changes in variable rates, CBA and NAB have also adjusted their fixed rates, increasing them by up to 0.30 and 0.35 percentage points, respectively. Currently, CBA’s lowest advertised fixed rate for a one-year term stands at 6.49 percent, while NAB offers a rate of 6.04 percent for the same period.

Meanwhile, ANZ’s most competitive advertised fixed rate is currently at 5.99 percent, reflecting the broader trend of rising interest rates in the market.

ANZ’s lowest advertised fixed rate is hovering at 5.99 per cent.

Westpac customers won’t be slugged with the rate hike until Tuesday, March 31.

It will offer the lowest advertised variable rate at 5.74 per cent once the new rates are in effect across all four big banks.

The only other big four bank offering an advertised variable rate under 6 per cent is CBA at 5.84 per cent.

Westpac also currently offers the lowest fixed rate, but that could change in the coming days.

Most mortgage holders will be hit with higher rates right away, which will sting when combined with the RBA’s February rate hike.

“Variable borrowers across the country are now having to brace for the second cash rate hike in as many months, while staring down the barrel of a potential third hike as soon as May,” Canstar data insights director Sally Tindall said.

Mortgage holders with a debt of $500,000 could pay at least $151 more per month with the cumulative increase from February and March, according to data from Canstar.

Those paying the minimum on their monthly repayments will have a few weeks to prepare for this latest rate increase before it hits.

That’s because the big four banks must provide written notice of the changes; at least 20 days’ notice for CBA, and at least 30 days’ for the other three.

“Make no mistake, banks are starting to charge customers higher rates from today, but be aware there’s a significant delay between today and when that extra money comes out of your bank account, for those paying the minimum,” Tindall said.

“Customers might think they’ve successfully accounted for two hikes, when in actual fact they might not have even started paying for the first one.”

Borrowers who can’t meet the higher repayment amount can request a rate review or rate reduction.

They can also contact their bank, which may be able to help them switch to interest-only or make reduced payments for a period of time, or extend the loan term.

The National Debt Helpline also offers free financial advice.

”There’s almost certainly more pain ahead for borrowers, with all four big bank economists forecasting another 0.25 percentage point hike in May,” Tindall said.

“If you’ve got a mortgage, work out what your repayments might look like if rates rose not just in May but again later in the year.

“You want to make sure this figure fits in your budget alongside the other rising cost-of-living pressures.”

NEVER MISS A STORY: Get your breaking news and exclusive stories first by following us across all platforms.

The information provided on this website is general in nature only and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information on this website you should consider the appropriateness of the information having regard to your objectives, financial situation and needs.