Share and Follow

in brief

- War in the Middle East has rattled energy markets and could push inflation further above the RBA’s target.

- It comes as Australians are devoting a bigger share of income to mortgages, new data suggests.

The Reserve Bank of Australia (RBA) is confronting an exceptionally tough decision regarding interest rates due to increasing inflationary pressures, exacerbated by the ongoing conflict in the Middle East, according to analysts.

Just a week prior, the consensus was that the RBA would maintain current interest rates at its March board meeting, concluding on Tuesday.

However, the situation shifted drastically with the outbreak of conflict in the Middle East, which has obstructed oil transport through the Strait of Hormuz. This disruption has led to significant upheaval in energy markets and has driven fuel prices to spike.

Experts caution that the price of oil could soon surpass US$150 per barrel, potentially causing inflation — currently at 3.8 percent — to deviate further from the RBA’s target range of 2-3 percent.

War ‘shock’ raises inflation risk

During a recent interview with The Conversation, RBA deputy governor Andrew Hauser expressed that the central bank is particularly wary about the persistence of high inflation.

“Failing to raise rates to the level they need to be and allowing inflation to get out of control is a clear problem,” Hauser said, adding there were also risks with acting “precipitously”.

HSBC chief economist Paul Bloxham said: “The market has taken this interview as guidance that a hike is more likely in March than not.”

Treasurer Jim Chalmers has also said scenarios were being modelled where inflation peaks at mid to high fours, due to the war in the Middle East

“The source of the most extraordinary volatility in our forecast and in the economy … is really how long this (war in the Middle East) drags out for,” he told Sky News on Sunday.

“We know already that it’s a very substantial shock.”

Will the RBA hike rates again?

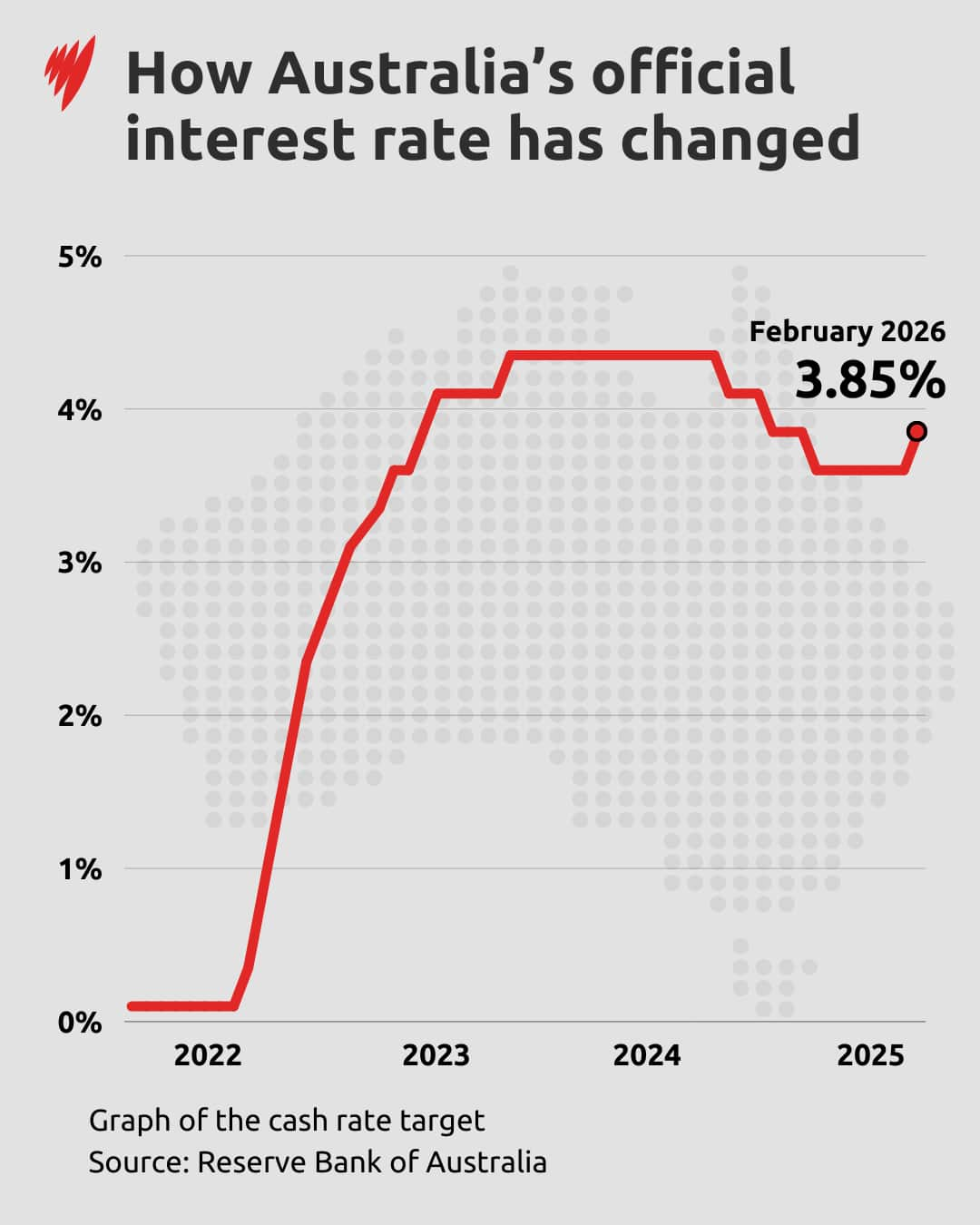

The RBA hiked the cash rate to 3.85 per cent at its February meeting, up from 3.6 per cent — a level it had been at since August after a 0.25 percentage point drop.

AMP chief economist Shane Oliver believes there will be more debate than usual at Tuesday meeting. While he believes interest rates should be left on hold, he said the RBA is likely to lift them.

“With uncertainty from the war in the Middle East and fuel costs, there could be members who want to wait for the dust to settle before a rate hike,” he said.

“But I think ultimately the decision will be to raise rates again to head off concerns that they’re going to lose further control of inflation.”

While the RBA’s decisions are often unanimous, Oliver said this month’s meeting is the “most complicated” in years.

“It’s a long gap until the next meeting in May … some board members may lean towards waiting, and others may lean towards moving earlier,” he said.

Borrowers brace for RBA’s decision

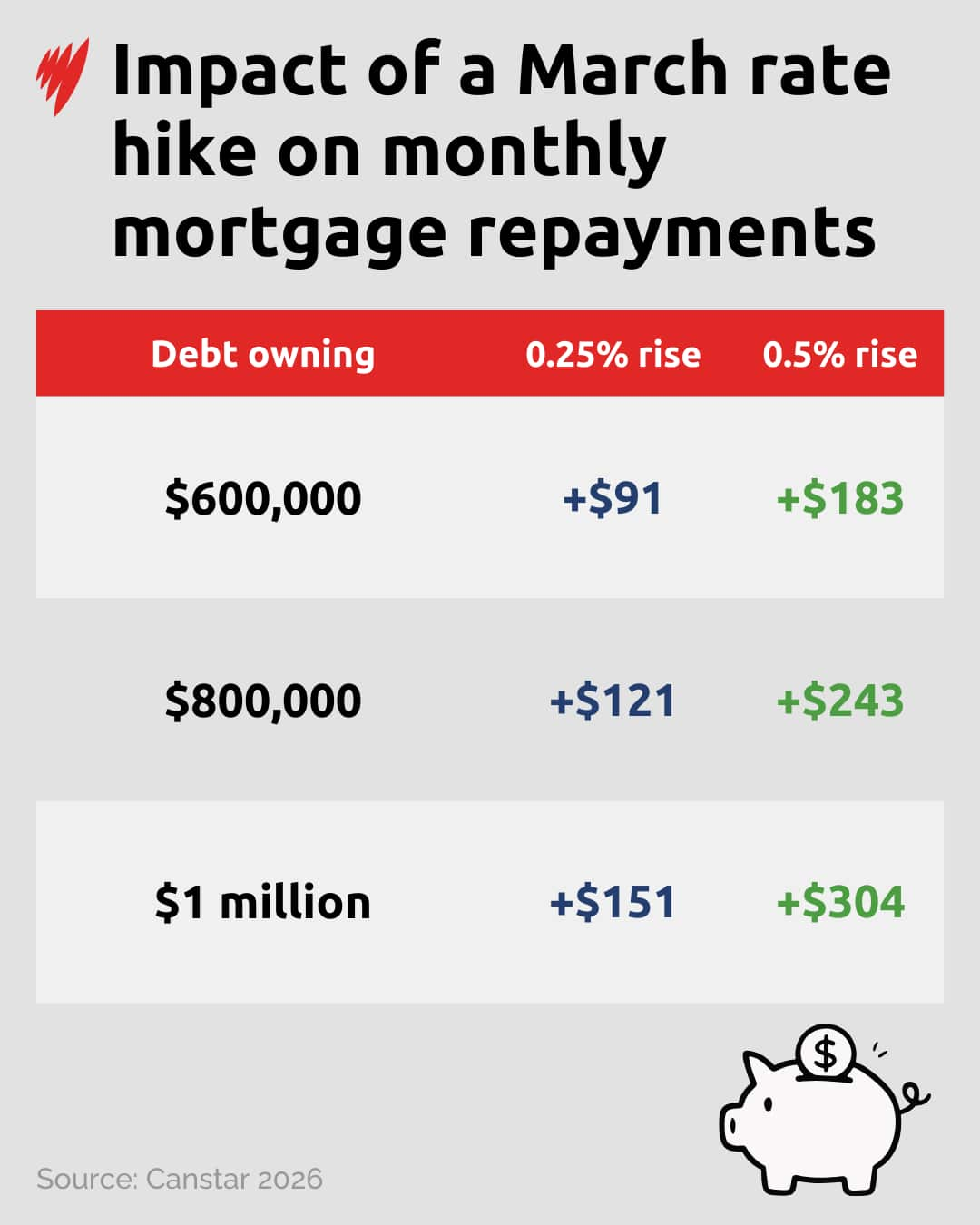

The imminent decision comes amid signs mortgage stress is on the rise and after a record jump in low-deposit lending — up 63 per cent ($2.1 billion) quarter-on-quarter in December, according to an analysis of Australian Prudential Regulation Authority figures by financial comparison site Canstar.

The lending increase follows the uncapping of the federal government’s First Home Guarantee scheme late last year — allowing first home buyers to purchase with a 5 per cent deposit rather than 20 per cent.

Canstar’s data insights director, Sally Tindall, told SBS News the uptick in lending shows people “aren’t having difficulty accessing credit”.

“But it also points to the fact that property prices are on the rise and continue to be on the rise, and that’s why people are taking on more and more debt,” she said.

Liv Cotterill is among those who have made use of the scheme, with it having made her buying power “so much better”.

The Sydneysider had been saving for nearly a decade and “renting forever” and had felt buying a home was a pipe dream.

“I’m in my mid-40s, and I’m single, getting something wasn’t even on my mind as a thing I’d be able to do,” she said, adding that she was “lucky” her mum was able to contribute to her saving “a bit” after previously having not been in a position to help.

Cotterill said her budget is tighter since collecting the keys for her property in December, with her mortgage repayments around double what she used to pay in rent.

She feels prepared for the RBA’s decision on Tuesday. But if the central bank hikes the cash rate again in May, she could feel the pinch.

“I think another rate increase for me, for example, will be fine. I can manage that still. I think if it gets to another one after that or any more, then I’m going to be a bit more of a pinch,” she said.

Other borrowers, however, could be in a more precarious position.

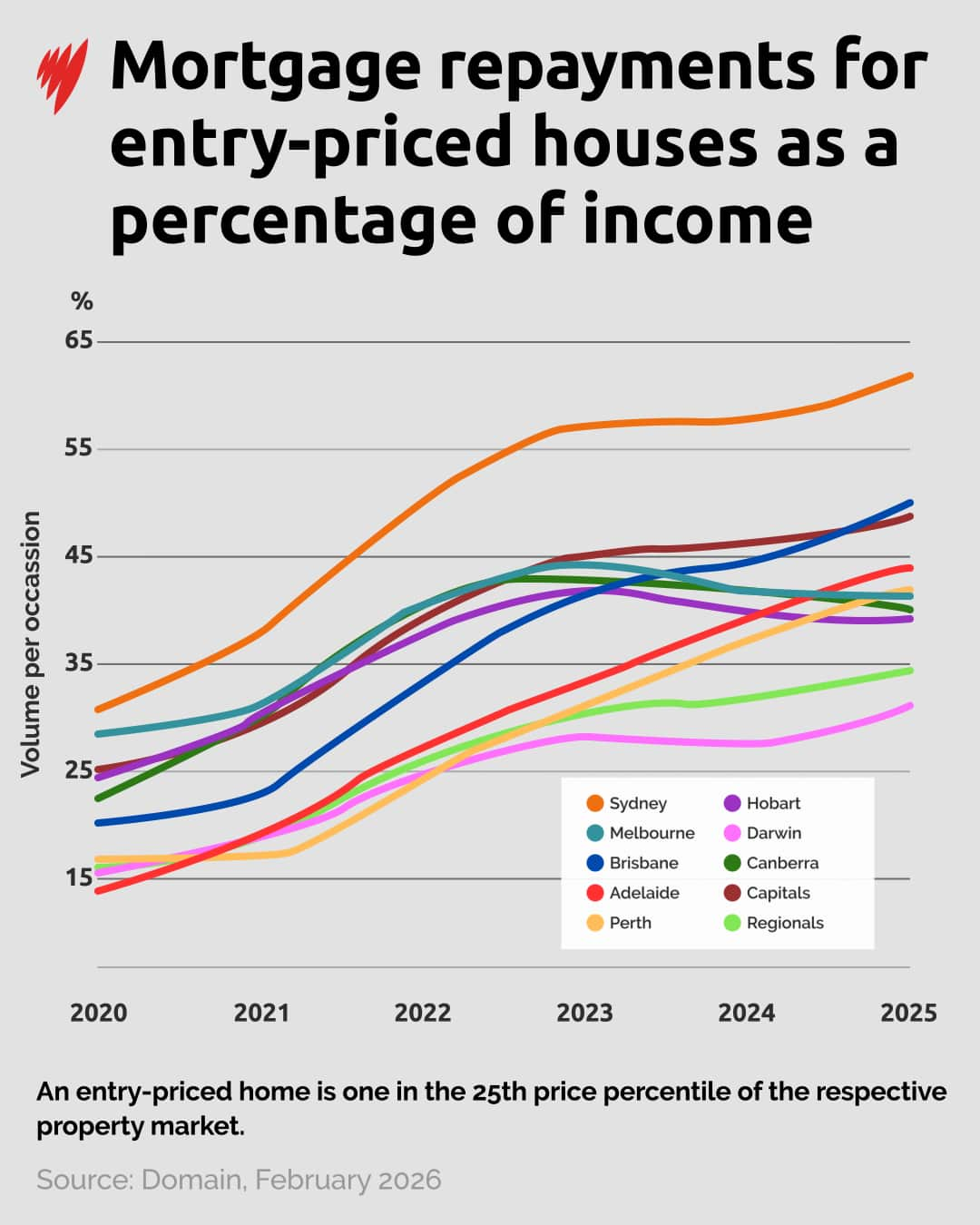

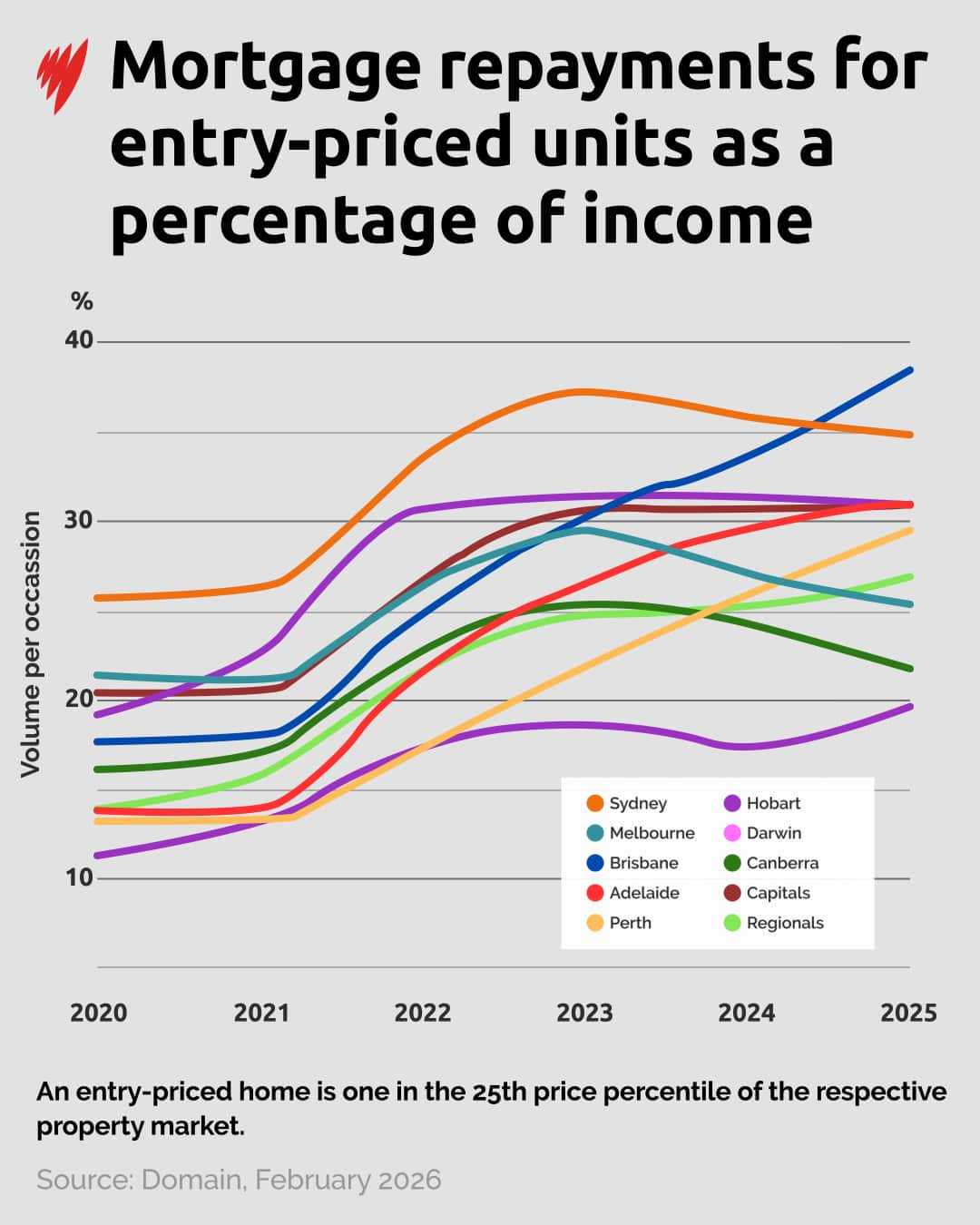

Data from Domain’s latest property report shows that Australians are spending a higher percentage of their income paying off their mortgage compared to five years ago.

The group defines a household as facing mortgage stress if it spends more than 30 per cent of its income on repayments.

Borrowers who own entry-priced houses in Sydney face the highest rates of financial stress, followed by Brisbane, then Adelaide and Perth.

“It’s quite extraordinary really, when you look at five years ago, where we saw pretty much no city in mortgage stress,” Domain’s chief of research and economics, Nicola Powell, said.

“Today, what we’ve got is all of our capital cities are in mortgage stress for entry houses.

“And when we’re looking at units, we’ve got Sydney, Brisbane, and Adelaide that are technically now in mortgage stress.”

— With reporting by the Australian Associated Press.

For the latest from SBS News, download our app and subscribe to our newsletter.