Share and Follow

in brief

- All four big banks expect the Reserve Bank of Australia to hike rates on Tuesday.

- A 0.25 percentage point hike in May would result in higher monthly repayments of $91 on a $600,000 mortgage.

The Reserve Bank of Australia (RBA) faces a challenging decision as it prepares for its Tuesday announcement. Most economists predict that the cash rate will likely be raised to 4.35%.

Recent data from the Australian Bureau of Statistics revealed that inflation surged to its highest point since the beginning of 2023 in March. This increase is partly attributed to the ongoing conflict in the Middle East, which has exerted significant pressure on prices.

A potential increase of 0.25 percentage points in the official cash rate would elevate interest rates from 4.1%, reverting them to levels seen in 2024.

This anticipated hike could negate the benefits of the previous three rate reductions, resulting in increased mortgage repayments for homeowners.

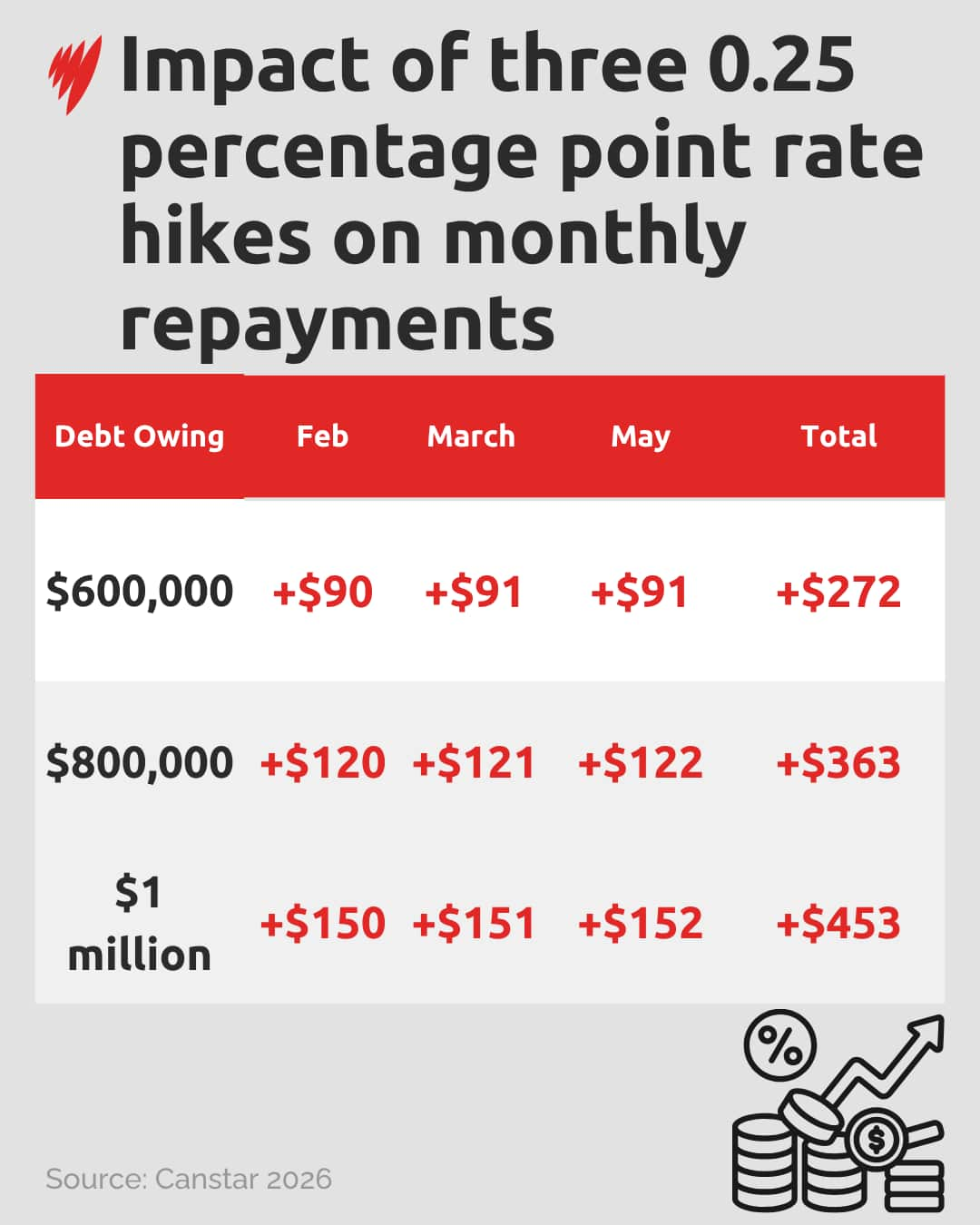

According to an analysis by financial comparison site Canstar, a 0.25 percentage point rise on Tuesday would mean an additional $91 in monthly payments for those with a $600,000 mortgage.

If the RBA decides to increase the cash rate, it will be the third hike this year, totalling a $272 rise in monthly repayments on a $600,000 mortgage compared to 2025.

Canstar data insights director Sally Tindall told SBS News a rate increase would create “significant pressure” for borrowers.

Tindall explained the board will be looking to reduce inflation to below 3 per cent.

The March figures showed inflation surging from 3.7 per cent to 4.6 per cent.

The RBA targets a 2-3 per cent inflation band and uses interest rate increases to cool discretionary consumer spending. Banks pass on the cash rate rise to borrowers, and mortgage payments increase as a result.

In light of rising costs and overseas conflict, Tindall said a hike could tip financially vulnerable Australians over the edge.

“The last (RBA) board decision was split five to four. If one person around that board table last time around had a different view, we might’ve ended up with potentially a hold rather than a hike,” Tindall said.

“I can only imagine it’ll be yet another split decision that comes down to the wire because of these competing factors.”

Confidence drops as repayments increase

Tindall said that consumer confidence has been falling in 2026, driven by tough and uncertain economic conditions.

This has resulted in a market slowdown, with people being more cautious about buying or selling property.

Current homeowners would be the most impacted in the short term by an anticipated hike.

“A cash rate hike could be the straw that breaks the camel’s back,” she said.

“For new borrowers, who potentially might not have even been expecting any cash rate rises after last year’s drops, they could have a wake-up call.”

Australians with a larger mortgage debt will pay more over the lifetime of their mortgage.

A homeowner with $800,000 in debt would pay an additional $363 each month, and those with $1 million in debt would owe $453 more in monthly repayments.

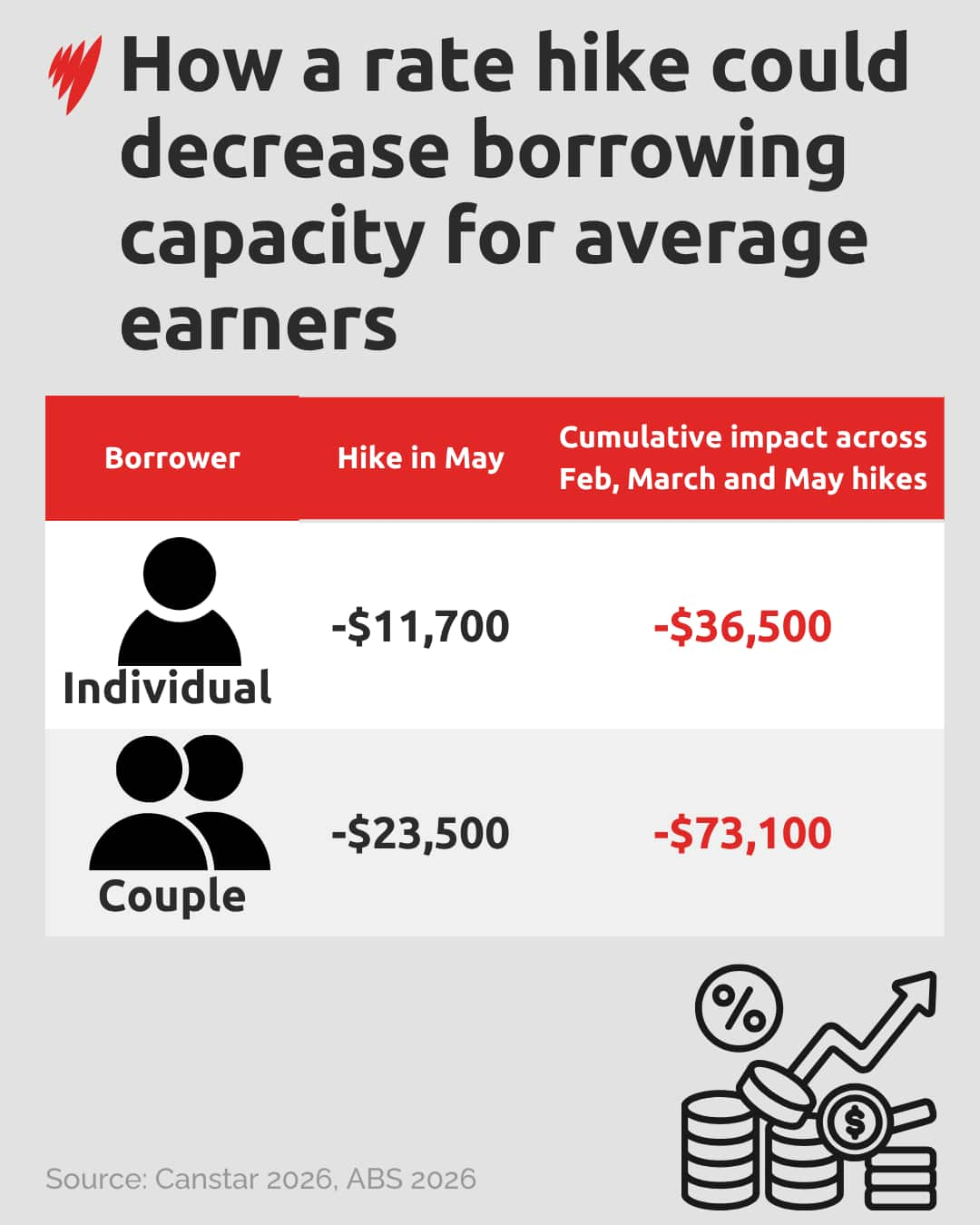

Rate hikes have also affected buying power.

An individual borrower with an average full-time wage of $106,950 will be able to borrow an estimated $11,700 less if an RBA rate rise materialises on Tuesday.

Combined with the previous February and March rate hikes, this borrower would be $36,500 worse off.

While all four big banks expect a hike on Tuesday, Westpac does not expect the cash rate hikes to stop there, forecasting two further 0.25 percentage hikes in June and August.

Risks of another rate hike

While the RBA is tipped to raise rates once again, financial services firm Betashares’ chief economist David Bassanese said it could be reluctant to do so.

“Much will depend on how long the Iran conflict persists and whether the Strait of Hormuz remains effectively closed,” he said.

“A more serious energy squeeze could emerge if the Strait is not reopened within the next month as existing oil inventories begin to run down.”

United States President Donald Trump said a project will start on Monday to help stranded ships leave the Strait of Hormuz, but offered few details.

Around 20 per cent of global oil exports ordinarily travel through the Strait.

Another risk the RBA may need to consider, Bassanese added, is “potential fallout” for the property market from changes to tax incentives in the upcoming budget.

“A combination of reduced tax incentives and multiple rate hikes could knock the wind out of the housing market, with negative wealth effects for household demand,” he said.

For the latest from SBS News, download our app and subscribe to our newsletter.